The Loan Estimate is intended to provide a clear and concise summary of the terms and costs associated with any loan. Here’s how to read it with confidence.

The Loan Estimate (LE) provides a clear and concise summary of the terms of your loan to help you understand the features, costs and risks associated with your mortgage as required by the Consumer Finance Protection Bureau (CFPB). Before moving forward with any lender, you should be sure to compare and understand your Loan Estimate.

Your initial LE

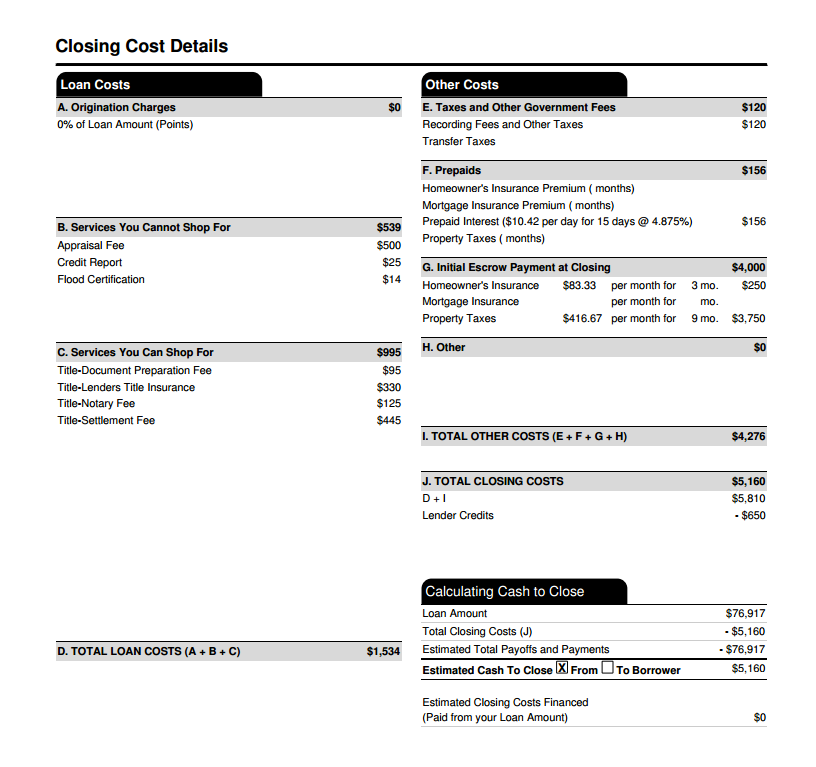

This is page 2 of sample LE in the CFPB-approved format. Make sure your lender provides an estimate in this format. Anything that looks different is not an official Loan Estimate.

Page 2 of the LE details your loan costs

Tips for comparing LEs from different lenders

Here are a few things to look out for:

1. Third-party fees appearing on one lender’s LE and not another’s

You should raise this with your Mortgage Expert. While the fee amount can vary, the types of third-party fees associated with a loan are fairly constant. One lender may be missing something.

2. Differences in loan amount for a refinance

A lender may increase your loan amount slightly to create a “no closing cost loan”. Borrowing a little more than the payoff on your current loan is one way to offset fees at the closing table, but this is increasing your debt to pay for your closing costs; it does not make them go away. For an apples-to-apples comparison across lenders, you should get LEs with identical loan amounts.

3. Promises of credits after close that do not appear on the LE

This is a major red flag. The purpose of the LE is to create transparency and accountability. You lose both by transacting outside of the standard disclosure.

4. Increasing costs during a change in circumstance

Some lenders may advertise attractive rates and fees for one product, then switch into something less competitive (bait-and-switch). You should ask about any additional fee and look at the relative competitiveness of the new product by continuing to shop before locking.

A Better way

Better Mortgage is committed to a transparent and efficient mortgage process. Contact us by email (hello@better.com), phone (888-501-3186), or chat with us via Better.com with any questions about your LE. We are happy to walk you through competing offers and answer any questions. No pressure, no sales — just a fast, easy and transparent process.