What You’ll Learn

Who are interested parties

What qualifies as a contribution

How contributions affect your mortgage

Before you send out invitations to your housewarming party, you’ll need to know about interested parties. Believe it or not, there are a lot of people who want you to buy the house you’ve been eyeing. Within the context of your future loan, these people are called “interested parties,” and they help incentivize your purchase by contributing credits to your transaction. That’s where we get the term “interested party contributions.”

The two most common interested party contributions (IPCs) are real estate agent or seller credits. Seller and real estate agents will offer to help out with taxes, a few months of property insurance, or any number of closing costs to help you buy your new home.

These credits are applied through closing and are factored into the final closing disclosure. When applied, these credits may affect your loan to property value ratio (LTV), which can then force you to incur further costs like mortgage insurance premiums.

Don’t fret, though. We’re here to help. Let’s take a look at how IPCs can help and how we can keep them from hurting.

Here’s the lay of the LTV land:

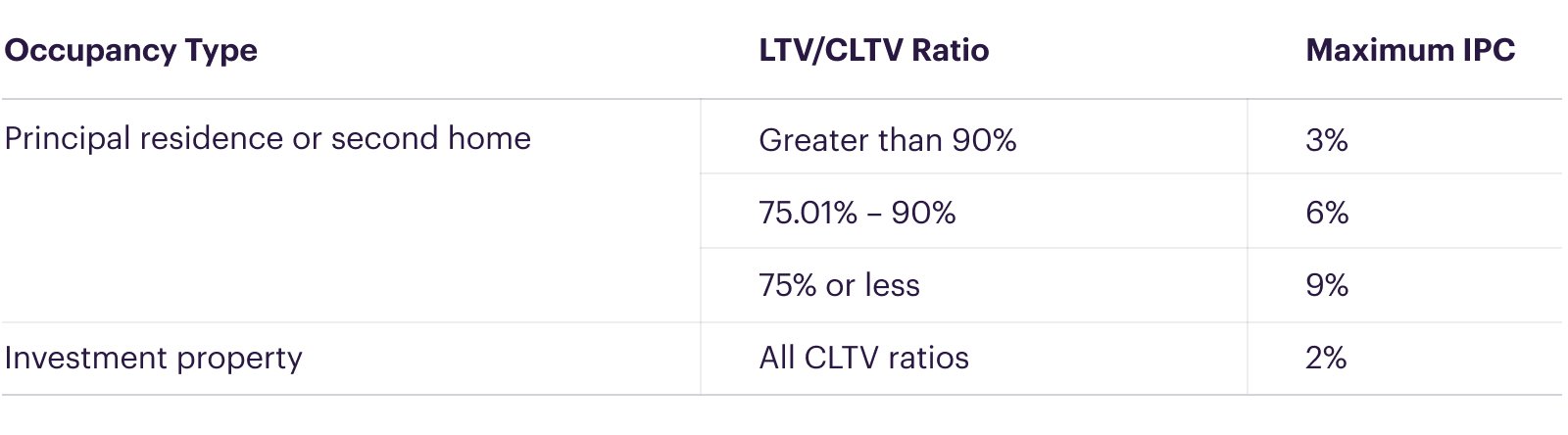

For mortgages that adhere to Fannie Mae guidelines, or conforming loans, there are maximum IPCs. The smaller the loan to value ratio (LTV), the more you can receive in interested party contributions (IPC). Essentially, Fannie Mae wants to make sure that people aren’t being wooed with credits and that they can make good on their mortgage agreement 5-30 years in the future.

— For LTV greater than 90%, the maximum IPC is 3% of the purchase price or the total closing costs, whichever is less.

— For LTV greater than 75%, but less than or equal to 90%, the maximum IPC is 6% of the purchase price or the total closing costs, whichever is less.

— For LTV less than or equal to 75%, the maximum IPC is 9% of the purchase price or the total closing costs, whichever is less.

— For Investment properties, the maximum IPC is 2% of the purchase price or total closing costs, whichever is less. LTV does not impact this.

Watch out for excess credits

Here’s where it gets a little tricky. If your seller or real estate agent is generous, and their IPC exceeds the maximum amount, the excess credits will be recorded as a reduction in purchase price.

That sounds great, but by lowering your purchase price, your LTV ratio will shift. If your LTV becomes greater than 80%, you will have to purchase mortgage insurance, and that will be more expensive in the long run.

So before you sign on the dotted line, it might help you to talk with your interested parties to see if their contributions will help you in the long run.

Let’s take a look at some “real life” applications

Here are a few hypotheticals that show you how IPCs can complicate closing costs.

Example 1

A $250,000 Purchase with a $150,000 Loan would be a Loan to Value Ratio (LTV) of 60%.

At 60% the maximum IPC would be 9% of the purchase price, $22,500, or the closing costs, whichever is less.

If the IPC, be it from seller or realtor, were to be $25,000 the credit would exceed the IPC limits. As such, the excess $2,500 would be a sales concession. The purchase price would be considered as $247,500 ($250,000-$2,500) and the resulting LTV would be 60.61%. This change in LTV can affect loan terms in some cases, but shouldn’t cause you to buy mortgage insurance.

Example 2

A $250,000 Purchase with a $200,000 Loan would be a Loan to Value Ratio (LTV) of 80%.

At 80% the maximum IPC would be 6% of the purchase price, $15,000, or the closing costs, whichever is less. Assuming closing costs are above $15,000, if that same $25,000 credit from example 1 was offered, the $15,000 cap would leave $10,000 unused credit. The purchase price would be considered as $240,000 ($250,000 minus $10,000) and the resulting LTV would be 83.33%. This change in LTV may significantly affect the loan terms since mortgage insurance would now be required.

Example 3

A $250,000 Purchase with a 200,000 Loan would be a Loan to Value Ratio (LTV) of 80%.

At 80% the maximum IPC would be 6% of the purchase price, $15,000, or the closing costs, whichever is less. In this example we will assume a credit of $10,000 and closing costs of $8000. In this case since the closing costs are the limiting agent, your closer will verify final closing costs and cap the credit at the total of the closing costs.

It helps to strategize with a pro

Closing costs tend to shift after IPCs are applied. Consult your Loan Consultant before closing for advice on how best to manage excess credits.