Here’s a look at the latest developments in the refinance market this week.

What rising inflation means for refinance rates, and where they could go from here

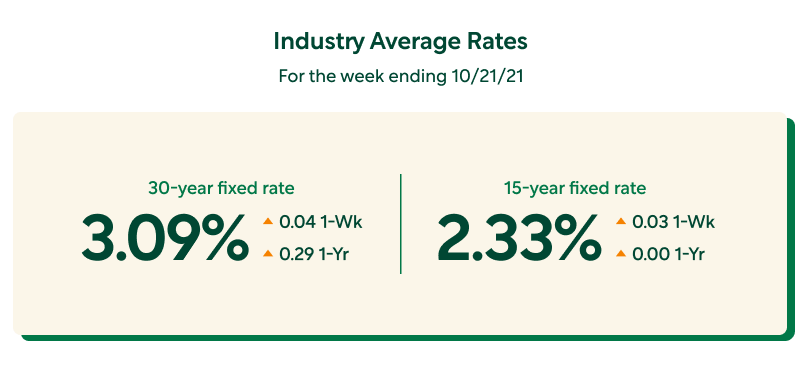

Rates are on the rise, but they’re still low compared to pre-pandemic months. The 30-year fixed rate mortgage rose 0.04% last week to an average of 3.09%. For context, the rate hovered closer to 3.50% at the start of last year.

There are a number of factors that affect mortgage rates, but a large driver for today’s rise is inflation. Inflation refers to an increase in the prices of goods and services around the country, and how it relates to people’s ability to purchase them. If the goods and services you spend money on each year rose by 2% on average, it would mean 2% inflation. In other words, your income last year would buy 2% less at today’s prices. That’s a healthy rate of inflation, according to The Federal Reserve.

Today, inflation is on the rise and likely to stay that way until the middle of next year. That drives mortgage rates up because investors on the market expect lenders to increase their rates to align with their return on a loan. Between now and the end of the year, Better Mortgage analysts expect that rates will keep going up, but likely won’t pass 3.25%.

Getting the ball rolling on a refinance can likely save you more than trying to time the market. Get your personalized rates and estimated payments in minutes, with zero obligations or impact to your credit score. You may even be eligible for programs like RefiNow and RefiPossible, which are estimated to save up to $3,000 per year.

15-year rates are lower than 30-year rates—is a shorter loan term right for you?

Shorter loan terms often carry lower interest rates than the popular 30-year mortgage. This week is no exception, with the 15-year fixed rate average at 2.33% and the 30-year average at 3.09%. While a lower rate doesn't always mean more savings, there are benefits to a shorter term that could help you get more out of a refinance.

A shorter term often means higher payments, so a 15-year loan can be a good choice if you’ve got some wiggle room in your monthly budget. On the flipside, you’ll build home equity faster, because a larger portion of each payment is going towards the principal—the amount you borrowed—rather than interest. On a 30-year mortgage, monthly payments may be lower, but there is more going towards interest. To get a closer look at how your payments break down, try the Better Mortgage amortization calculator.

The 15-year mortgage term usually comes with fewer upfront costs, too. They’re often exempt from the loan-level price adjustment fees that Fannie Mae and Freddie Mac can require for 30-year loans, and may come with lower insurance premiums.

It all depends on your finances, priorities, and goals for a refinance. Read our guide to 15- and 30-year fixed rate loans to weigh your options, and find out what you can expect to pay for each term by seeing your personalized mortgage rates.

Considering a home loan?

Get your custom rates in minutes with Better Mortgage. Their team is here to keep you informed and on track from pre-approval to closing.